How to Pay Off Your Mortgage 10 Years Early and Save Over $100,000 in Interest

How to Pay Off Your Mortgage 10 Years Early and Save Over $100,000 in Interest: A Guide for Northeast Ohio Homeowners

Introduction

For many Northeast Ohio homeowners, paying off your mortgage early may feel like a dream—one that seems too good to be true. But what if there were a simple, proven strategy to shave years off your mortgage and save tens of thousands of dollars in interest? It’s possible, and you don’t need to be a financial wizard to make it happen.

In this post, we’ll explore a practical approach to mortgage repayment that could change your financial future. By making strategic extra payments, you’ll not only save a substantial amount in interest but also gain the peace of mind that comes with being debt-free. Whether you’re looking to build wealth or simply reduce financial stress, this strategy is for you.

Key Takeaways

Extra Payments on Principal: Paying extra toward your mortgage principal can significantly reduce the interest you pay over the life of your loan.

Amortization Advantage: Understanding and leveraging your mortgage amortization schedule is crucial to maximizing savings.

Guaranteed ROI: Extra payments can yield a guaranteed "return on investment" of hundreds of percent.

Eliminate Years of Payments: Consistent extra payments can shave a decade or more off your mortgage term.

Free Resources: Learn how to set up this system with our complimentary course.

Why Paying Off Your Mortgage Early is a Smart Financial Move

The Myth About Low-Interest Rates and Tax Deductions

A common misconception is that low-interest rates and tax deductions make it unwise to pay off a mortgage early. While these factors do provide some benefits, the massive savings in interest from early repayment often far outweigh these perceived advantages. Plus, as you pay off your mortgage, you’re freeing up money that could be invested elsewhere.

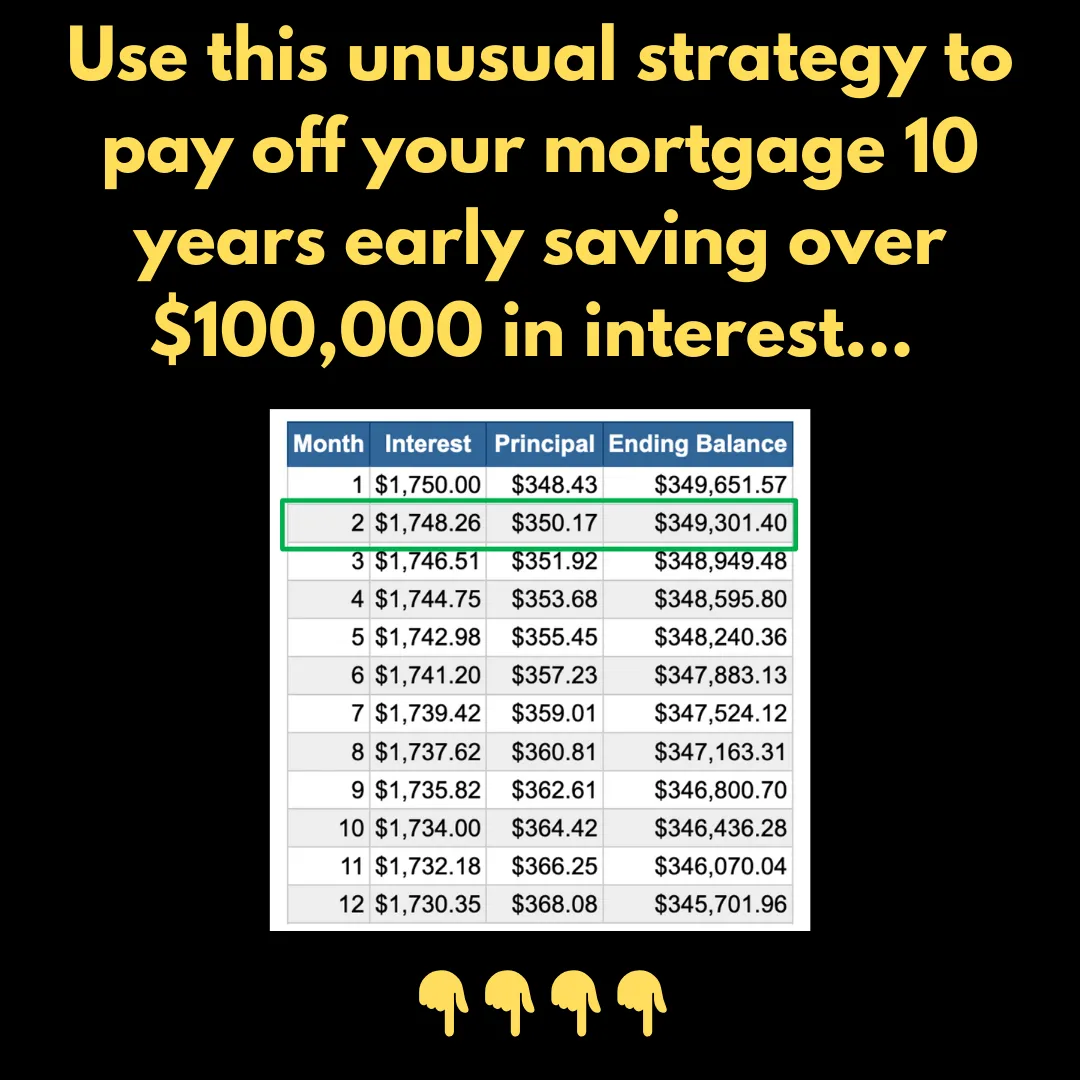

The Reality of Amortization Schedules

Traditional amortization schedules are structured to favor lenders. For a $350,000 mortgage at 6% interest, the majority of early payments—83%, to be exact—go toward interest rather than reducing the principal. For example, on a $2,098 monthly payment, only $348 goes to the principal in the first month. Over time, this imbalance shifts, but during the early years of the loan, homeowners pay a hefty premium in interest.

The Strategy: Making Extra Principal Payments

How It Works

The key to this strategy is simple: make the next month’s principal payment along with your current mortgage payment. For instance, if your principal payment for month two is $350, add that amount to your first mortgage payment. This reduces your outstanding balance more quickly, saving you thousands in interest over the life of the loan.

Real Savings Example

Let’s say you follow this plan for one year. By making additional principal payments every month, you could save over $20,000 in interest and eliminate 12 full mortgage payments. That’s like getting a two-for-one deal on your monthly payments!

A Guaranteed Return on Investment

Unlike the stock market or other investments, this strategy offers a guaranteed return. For every $350 extra principal payment, you could save $1,748 in interest. That’s a 400% return—virtually unheard of in traditional investment vehicles.

Automating Your Extra Payments

The best part? You don’t have to pay for this yourself. With smart financial planning, such as leveraging rental income or side hustles, you can automate these extra payments. Many homeowners in Northeast Ohio have found creative ways to fund this strategy, effectively letting someone else help pay down their mortgage.

Conclusion

Paying off your mortgage early isn’t just a dream; it’s a goal well within your reach. By making strategic extra payments, you can save tens of thousands of dollars in interest, eliminate years of mortgage payments, and enjoy financial freedom sooner than you ever thought possible. If you’d like to learn more about setting up this system, reach out today for our free course. It’s time to take control of your mortgage—and your financial future.

FAQs

How much should I pay extra toward my mortgage each month?

Start with the next month’s principal payment as an extra amount. Over time, increase it if your budget allows.

Does this strategy work with all types of mortgages?

Yes, though it’s most effective with fixed-rate mortgages. Adjustable-rate mortgages (ARMs) may require additional consideration.

What if I can’t afford extra payments every month?

Even sporadic extra payments can make a big difference. Start small and increase as your finances allow.

Will my lender penalize me for paying off my mortgage early?

Check for prepayment penalties in your loan terms. Most modern mortgages do not include these penalties.

How does this impact my credit score?

Paying off your mortgage early has no negative impact on your credit score. In fact, it may improve your score over time.